Perpetual Futures Contracts and Cryptocurrency Market Quality: Insights from Emerging Markets

By Qihong Ruan and Artem Streltsov, PhD candidates

Bitcoins. Image by Ashley_Jackson from Pixabay.

Why perpetual futures matter

Perpetual futures contracts, or “perps,” are a financial innovation that allows traders to speculate on cryptocurrency prices without an expiration date. Unlike traditional futures, which settle on a fixed date, these contracts can be held indefinitely. Economist Robert Shiller first proposed this concept in 1993, but it has only recently gained widespread use—dominating the cryptocurrency derivatives market, accounting for 93 percent of all crypto derivatives trading.

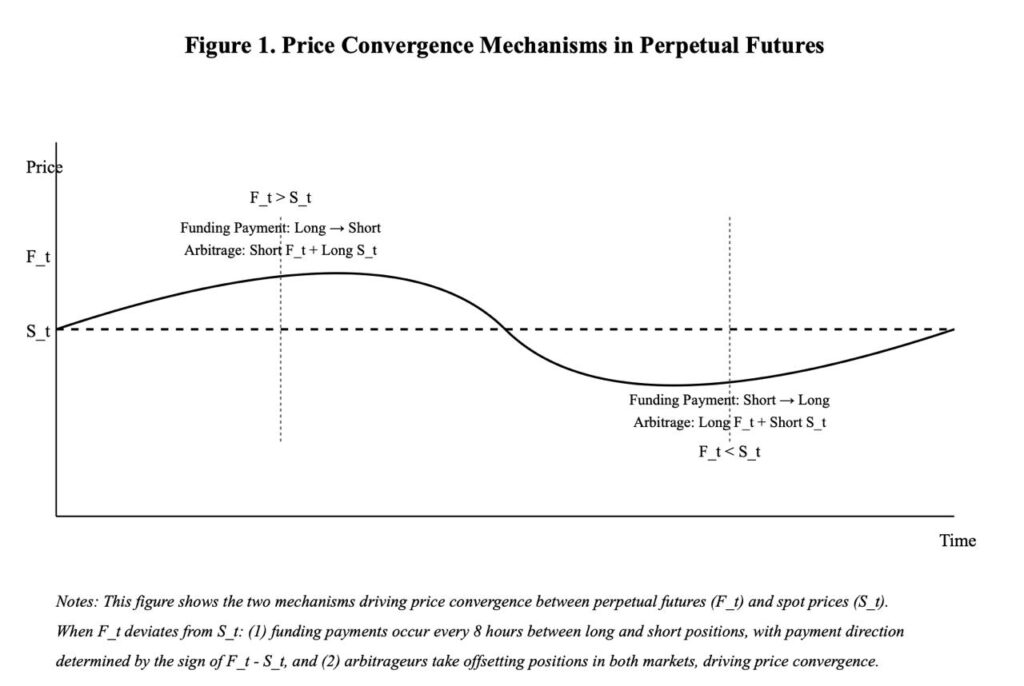

The most distinct feature of these contracts is their eight-hour funding fee mechanism, where traders periodically pay or receive a small fee to align the contract price with the underlying spot market. While widely adopted, these contracts are still poorly understood in terms of their impact on market structure—especially in emerging markets, where cryptocurrency adoption is growing rapidly.

Diagram illustrating the funding fee mechanism in perpetual futures contracts. From our paper “Perpetual Futures Contracts and Cryptocurrency Market Microstructure”

How perpetual contracts reshape crypto markets

Our research investigates how perpetual contracts impact cryptocurrency market behavior. We highlight three key effects:

- Increased trading activity: Since perpetual contracts allow 24/7 leveraged trading, they dramatically boost market participation

- Higher trading costs: The funding rate mechanism and leverage increase trading expenses, making markets more liquid but also costlier

- Enhanced informed trading: With access to leverage and short-selling, sophisticated traders can act aggressively on their information, influencing market efficiency

Our research approach and findings

To isolate the impact of perpetual contracts from general market fluctuations, we adopted three distinct research strategies:

- The eight-hour funding cycle as a natural experiment. Because perpetual contracts require funding fee payments every eight hours, we analyzed market behavior during these cycles. We found that both trading activity and bid-ask spreads follow a U-shaped pattern within each cycle. The fact that this pattern appears in both perpetual and spot markets suggests that the contracts actively shape market behavior rather than merely responding to existing trends.

- Staggered adoption of perpetual contracts. We also studied what happened when different crypto exchanges introduced perpetual contracts at different times. Consistently, we observed higher trading volume and wider bid-ask spreads following their introduction, reinforcing our conclusions.

- The Chinese cryptocurrency ban—a natural experiment. In September 2021, the People’s Bank of China (PBOC) banned cryptocurrency activities, forcing Huobi—one of the largest exchanges—to suspend perpetual contracts while competitors like Binance, OKEx, KuCoin, and Bibox continued offering them. This policy change created a natural experiment, allowing us to measure the effects of removing perpetual contracts.

We observed that after Huobi halted perpetual contracts:

- Trading volume declined, suggesting that perps are a major driver of crypto market activity

- Trading costs fell, implying that their presence raises transaction expenses

- Fewer sophisticated traders participated, indicating that these instruments are crucial for informed market participants

These findings provide strong causal evidence that perpetual contracts fundamentally change market dynamics.

How perpetual contracts benefit informed traders

Perpetual contracts provide informed traders with powerful tools:

- Leverage: Allowing traders to amplify their positions beyond their initial capital

- Short selling: Enabling profit from falling prices, improving market efficiency

- 24/7 trading – Unlike traditional stock markets, crypto markets never close, creating continuous arbitrage opportunities

Because informed traders gain a competitive edge, market makers react by widening bid-ask spreads, increasing trading costs.

Real-world validation: The Walmart-Litecoin incident

To further validate our findings, we examined an independent market event—the false news in September 2021 that Walmart would accept Litecoin as payment. The announcement briefly caused Litecoin’s price to surge 30 percent, only to collapse once the news was debunked.

While this incident did not involve perpetual contracts, it provided a case study of how informed traders capitalize on market inefficiencies, reinforcing our broader conclusions.

Our findings are critical for policymakers in emerging economies, where cryptocurrency trading is becoming mainstream. Perpetual contracts:

- Boost market efficiency by enabling informed trading

- Increase trading costs, making participation more expensive

- Create regulatory challenges, as they introduce new risks and volatility

As Shiller originally envisioned, similar contract structures could be applied beyond cryptocurrency, including:

- Real estate derivatives to hedge property values

- Human capital financing through income-sharing agreements

- Economic indices, providing innovative risk management tools

Understanding their role in cryptocurrency markets offers valuable insights for future financial applications.

Acknowledgments

We are grateful to the Emerging Markets Institute for research support, as well as the following organizations for funding and guidance:

- Cornell SC Johnson College of Business

- Fintech at Cornell initiative

– Digital Economics and Financial Technology Lab

– University Blockchain Research Initiative - Initiative for CryptoCurrencies and Contracts

About the authors

Qihong Ruan is a PhD candidate in economics at Cornell University, researching market microstructure, cryptocurrency trading, and AI-driven financial applications.

Artem Streltsov is a PhD candidate in finance at Cornell University, focusing on corporate finance, AI applications in finance, and market microstructure.