Stablecoins: Importance in Emerging Markets and Recommended Regulatory Framework

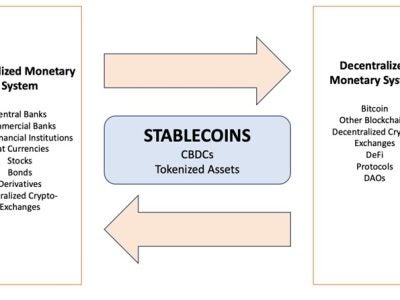

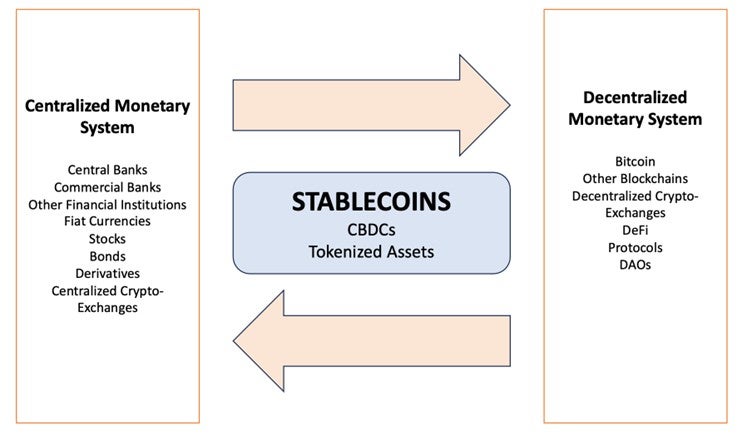

Stablecoins will become the bridge (with other virtual assets) between the centralized and decentralized financial systems. Image creation: Carlos Eduardo Bernos Amoros

Stablecoins represent a subset of virtual assets pegged to specific assets or baskets of assets like the U.S. dollar, gold, commodities, or contracts on other cryptocurrency assets. Unlike traditional cryptocurrencies, which are subject to market volatility, stablecoins aim to maintain price stability. However, their stability is relative, making the establishment of a comprehensive regulatory framework a challenging endeavor. Organizations considering the integration of stablecoins into their operational framework should prepare for evolving regulations.

Relevance for Emerging Markets

While Bitcoin has evolved from an unconventional investment to a store of value in the U.S. and Europe, stablecoins have emerged as a compelling option for cross-border payments and wealth preservation in non-dollarized economies. As high inflation rates erode savings, a common strategy is to rely on the U.S. dollar. However, banks and other financial institutions often provide limited solutions in these economies, making stablecoins a vital alternative for the average person in emerging markets. This highlights the growing importance and utility of stablecoins in providing economic stability and accessibility where traditional financial systems fall short.

Regulatory Landscape Overview

- United States: While the Securities and Exchange Commission may classify stablecoins as securities under certain conditions, various regulatory bodies like the Commodity Futures Trading Commission and the Options Clearing Corp. have distinct views on stablecoins, treating them as commodities or providing guidelines for banking activities, while the IRS taxes them as property.

- Europe: The European Securities and Markets Authority monitors stablecoins under the broader classification of crypto-assets, applying the Markets in Crypto-Assets regulation. The European Central Bank assesses stablecoins as potential payment systems.

- Asia: The Monetary Authority of Singapore treats stablecoins as digital payment tokens with specific requirements. In Japan, the Financial Services Agency requires issuers to maintain equivalent reserves. China, however, has banned stablecoin transactions as part of its broader prohibition on cryptocurrency.

- Latin America: Countries like Argentina and Brazil recognize the potential of stablecoins for remittances and anti-inflation measures. The Central Bank of Brazil views stablecoins as financial assets and explores regulations for integration.

This patchwork of regulatory measures, originally designed for traditional finance, has been adapted to the unique challenges presented by virtual assets, sometimes leading to inconsistencies. Establishing a universally accepted definition and categorization of stablecoins would be a fundamental step toward ensuring their security and operational efficiency. International regulatory collaboration is essential to develop a cohesive global framework.

Market Data Analysis

From 2021 to 2025, the market for stablecoins, specifically focusing on Tether (USDT), experienced significant growth. Tether’s market capitalization soared to over $141.4 billion, which indicates a robust expansion within the stablecoin sector. USDT continues to hold a dominant position in the stablecoin market, which surpassed $204 billion. This leadership is underpinned by its widespread use on centralized exchanges and in decentralized finance (DeFi) protocols, despite the controversies surrounding its reserves. Meanwhile, USD Coin (USDC) also showed notable growth, with its market capitalization increasing by 48%, reaching $52.5 billion, driven by its transparent reserve management strategy.

According to blockchain firm Chainalysis’s 2024 Geography of Crypto Report, India, Nigeria, and Indonesia stand out as the top countries in these emerging markets for their high levels of stablecoin usage. India is leading in overall and retail-sized cryptocurrency transactions, including those involving stablecoins. Nigeria is not far behind, particularly noted for using stablecoins to enhance cross-border payments and preserve wealth against currency devaluation. Indonesia also ranks high, primarily using stablecoins in DeFi applications.

Future Regulatory Trends and Recommendations

Looking ahead, stablecoin-related projects should prepare for increased regulatory focus on:

- Transparency: Stablecoin issuers will likely be required to disclose their reserve parameters and undergo regular audits. Companies utilizing stablecoins must outline scenarios in which the 1:1 peg may be compromised and establish contingency plans to protect users. In addition, regulators may introduce standardized reporting requirements to ensure consistency in how reserve data is presented across different issuers.

- Stabilization: Issuers should define the thresholds under which a stablecoin maintains its stability. If an asset fails to meet these criteria, it should not be classified as a stablecoin. Future regulations should distinguish between relative stability (e.g., USDC compared to Bitcoin) and absolute stability (e.g., USDC alone). Companies integrating stablecoins must incorporate stabilization clauses into their terms and conditions. Moreover, developing risk management strategies, such as capital buffers and liquidity reserves, will be crucial for issuers to sustain stablecoins’ value during market volatility.

- Scalability: Regulatory bodies should assess which industries and financial products are best suited for stablecoin adoption. High-risk industries such as gambling may face stricter limitations due to heightened anti-money laundering concerns. Meanwhile, sectors such as remittances and cross-border payments may see increased regulatory support due to their potential to enhance financial inclusion.

As stablecoins continue to evolve, it is crucial for businesses to remain agile, integrating sophisticated compliance controls and participating actively in regulatory discussions to navigate this dynamic sector effectively.

As virtual assets such as USDT or USDC, central bank digital currencies, and tokenized assets gain traction, they create a bridge that links traditional financial institutions with emergent financial technologies such as blockchain, decentralized exchanges, and DeFi protocols. This evolution indicates that stablecoins will likely play a crucial role in shaping the international financial system by offering a balance between the regulated security of conventional finance and the innovation and flexibility of decentralized models.

Stablecoins provide a stable medium of exchange that can be used across various platforms, reducing the volatility traditionally associated with cryptocurrencies like Bitcoin. This relative stability is essential for both everyday transactions and institutional investment, paving the way for greater adoption of blockchain technologies. As these technologies mature, the international financial landscape could shift, with stablecoins enabling seamless economic interactions across borders, enhancing transparency, and reducing transaction times and costs, leading to a more inclusive and efficient global financial system.

About the author

Carlos Eduardo Bernos Amoros is a second-year MBA student and an Emerging Markets Institute Fellow in the Samuel Curtis Johnson Graduate School of Management, specializing in fintech, blockchain, and cryptocurrencies. He is the cohost of Dentro del Bloque, a blockchain education podcast focused on Latin America with over 60 episodes. He has conducted research for the Cornell Brooks School Tech Policy Institute, examining the relationship between Bitcoin and financial freedom. Before joining the Johnson School, he worked in anti-money laundering compliance across the banking, fintech, and crypto industries.

The views expressed in the articles published on the Emerging Markets Institute webpage are those of the author(s) and do not necessarily reflect the views of the Emerging Markets Institute.

Article Information

- Categories

-

- Blog Posts