Scarcity of infrastructure a major obstacle to national economic growth

Private investors hesitate to invest in infrastructure in developing countries because of high level of political risk, exchange risk, and demand risk.

by HyungJoon (Simon) Kim

Based on my summer internship at Pacific Partnerships in New Zealand, I would like to suggest a new Multilateral Development Banks’ contribution model to boost transportation development in emerging countries. This suggestion has been induced through comparative analysis between advanced market and emerging market and between power sector and transportation sector. First and foremost, I really appreciate the generous funding of Roberto Canizares which made my summer internship possible.

Overview

Scarcity of infrastructure is a major obstacle to the national economic growth in most cases of emerging countries. It is true that Public-Private Partnership (PPP) has been regarded as a representative solution to the problem emerging market is facing. However, it seems hard to identify successful PPP projects in emerging market. This is because private investors hesitate to invest in infrastructure in developing countries because of high level of political risk, exchange risk, and demand risk resulting from low level of purchasing power. Nevertheless, private investment in power sectors is relatively active, compared to its investment in transportation sectors such as highways, railways, and ports.

Success factor of power sector

Aside from the fact that power (or electricity) is essential for the economic development, private sector has mainly invested in power sector in emerging countries in terms of risk profile. To be specific, power plant projects is based on Power Purchase Agreement (PPA) between private investors and government. In the case of power plant projects, demand risk, one of the biggest project risk that infrastructure projects have can be mitigated through a PPA. This is because government purchases the electricity at a specific rate based on the PPA. In this respect, unlike transportation projects which are exposed to demand risk, power plant projects can be free from demand risk. For this reason, private investors prefer power plant projects to transportation projects. In this context, in order to promote private investment on transportation projects, it can be considered to introduce a contract similar to PPA to the transportation sector.

Availability Payment

This type of contract is an Availability Payment (AP) contract. As a matter of fact, in advanced countries such as UK, Australia, Canada, and New Zealand, the AP has been applied in many transportation PPP projects. AP means that regardless of actual demand, government pays some money to the private investors as long as they satisfy the availability of the facility and quality of service. Therefore, private sectors can avoid demand risk in that they can recover their investment cost from the government’s payment. In other words, public sector (government) bears the demand risk, attracting the private sector’s investment. In this respect, AP is similar to PPA in the field of power sector.

Availability Payment mechanism: New Zealand example

When it comes to an actual example of Availability Payment in New Zealand, the mechanism is as follows. The government payment is calculated by the formula determined by negotiation between two sectors. As a big picture, the amount is divided into two parts; recovery of investment cost and its return, and reimbursement of operating expenses. Namely, two components have the following characteristics. The mechanism enables private investors to stably recover their investment and operate the facility during the asset’s whole life. For this reason, Availability Payment has been regarded as a standard model in advanced market.

[Characteristics of Two Components in AP]

| Item | Recovery of Investment Cost | Reimbursement of Operating Expenses |

| Period | Construction period | Operation period |

| Indexation | No Indexation | Indexation according to the sources |

| Trait | Investment Cost plus Return | Actually incurred expenses |

PPA mechanism: Indonesia example

As mentioned above, PPA mechanism is similar to the AP mechanism. In the case of hydro-power project in Indonesia, the government payment is composed of five components which can be categorized into two groups such as recovery of investment cost and reimbursement of operating expenses. So, the PPA mechanism is similar to the AP mechanism. As long as private investors satisfy the expected capacity and generate the expected electricity, there is no problem with stable recovery of investment and operation.

[Characteristics of Five Components in PPA]

| Item | Definition | Category |

| Component A | Capital Cost Recovery | Recovery of Investment Cost |

| Component B | Fixed O&M Cost Recovery | Reimbursement of Operating Expenses |

| Component C | Water Use Charges | |

| Component D | Variable O&M Cost Recovery | |

| Component E | Capital Cost Recovery for Transmission | Recovery of Investment Cost |

Introduction of Availability Payment mechanism to Emerging Market

As abovementioned, AP mechanism in New Zealand and PPA mechanism in Indonesia are similar in that both of them mitigate demand risk for private investors. The table below shows the comparison and similarity between two mechanisms. Thus, just as PPA mechanism in emerging countries’ power sector attracted private investors, so introducing AP mechanism in emerging countries’ transportation sector would be successful to boost private investment.

[Comparisons between AP and PPA]

| Item | New Zealand (AP) | Indonesia (PPA) |

| Structure | Recovery of Investment Cost + Reimbursement of Operating Expenses | |

| Payer | Government | |

| Demand Risk Taker | Government | |

| Difference | Payment depending on the Availability (Service Regime) | Payment depending on the actual generation |

In this regard, AP mechanism can be considered an alternative to encourage private sector to invest on transportation PPP projects in emerging market, as long as government can pay the amount to private investors on time. In both cases, both payer and demand risk taker are the government. However, in taking into account the financial capabilities of developing countries, it is probable that AP would not work in emerging countries. This is because basically most developing countries suffer from fiscal deficit. Thus, private investors would have concerns over government’s breach of contract or default on the ongoing Availability Payment. So, it is vital to improve the government’s capabilities regarding the Availability Payment.

Suggestion of new model with regard to MDB’s role

Thus, it is expected that Multilateral Development Banks (MDB) will be able to play a major role by subsidizing the government and securing the payment from the government. In this regard, it is a newly proposed model regarding MDB’s financial support for infrastructure development in emerging countries. The following table shows the difference between the MDB’s traditional loan method and proposed new model with regard to MDB’s participation. When it comes to the traditional PPP model, the investment cost is recovered by collection of toll charges from end-users. In this regard, this model is called patronage model. However, proposed new model means private investors recovers their investment cost through the Availability Payment from the government. These characteristics are closely related to who takes the demand risk.

[Comparisons between Two Models]

| Item | Traditional PPP method | Proposed new model |

| Type of project | Patronage model (Toll collection) | PPP model (Availability Payment) |

| Type of support | Financing of Investment Cost | Funding of Availability Payment |

| Period of use | Construction period | Operation period |

| Recovery method | Collection of Toll charges from End-users | Availability Payment from the Government |

| Payment method | MDB’s Disbursement based on the loan schedule | MDB’s Payment based on the AP schedule |

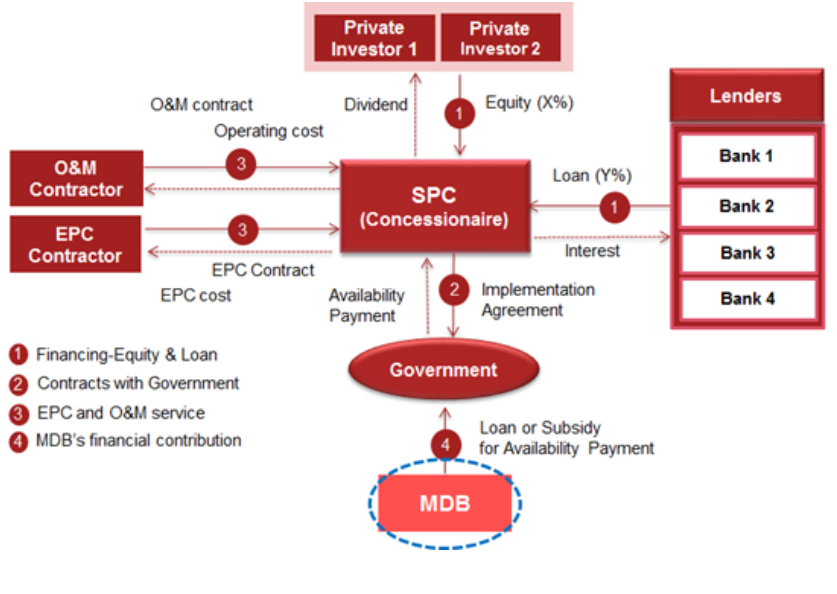

The following picture shows the structure of two models. The biggest difference between two models is MDB’s role, which is mentioned above. According to this new model, MDB contributes to Availability Payment during the operation period by providing loans or subsidy to the government of emerging countries, while in the case of traditional PPP model, MDB participated in financing by lending loans during the construction period. Compared to the traditional PPP model, proposed new model is more meaningful in terms of MDB’s role and function, since MDB on the new model is more essential to secure the business structure. As a matter of fact, MDB’s contribution on the traditional PPP model is restricted to partial participation in financing as one of lenders. Also, in reality, the amount of Availability Payment can be funded by MDB and government in the form of matching fund or by G to G (Government to Government) fund.

[Traditional PPP method]

[Proposed new model]

On top of that, according to the proposed new model, MDB’s role is not participation in financing but in funding. In some aspect, this new model is associated with combination of Availability Payment mechanism in advanced market and loan from MDB in emerging countries. This new suggestion implicates new change of MDB’s role in infrastructure development in emerging countries. Especially, it is expected that this new model will make a contribution to boosting investment on transportation projects in emerging countries.

Disclaimer: The views and opinions expressed in this article are those of the authors and do not necessarily reflect the views and position of any Emerging Markets Institute personnel.