3 reasons why robo-advisors threaten the traditional wealth management industry

By Gonzalo Bascur, One-Year MBA ’18

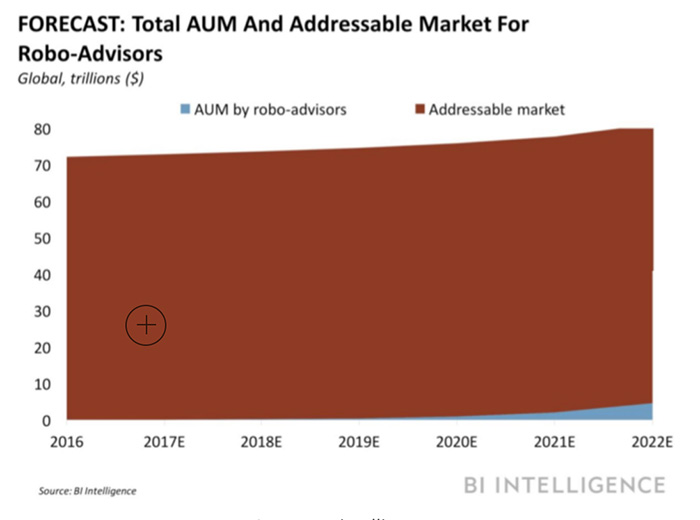

Have you ever considered the advice of a robot for your investments? It probably sounds weird, but it’s not at all. Robo-advisors are real, and they are giving advice right now. According to an A.T. Kearney simulation model, robo-advisors had $300 billion in assets under management (AUM) during 2016, and this figure is expected to increase by 68 percent CAGR until 2020. Despite this huge number, AUM by robo-advisors are far from their potential. According to Business Intelligence, AUM by robo-advisors are less than 1 percent of the total AUM globally. Though, the percentage of total AUM by robo-advisors within the global total AUM are expected to be more than 3 percent by 2022.

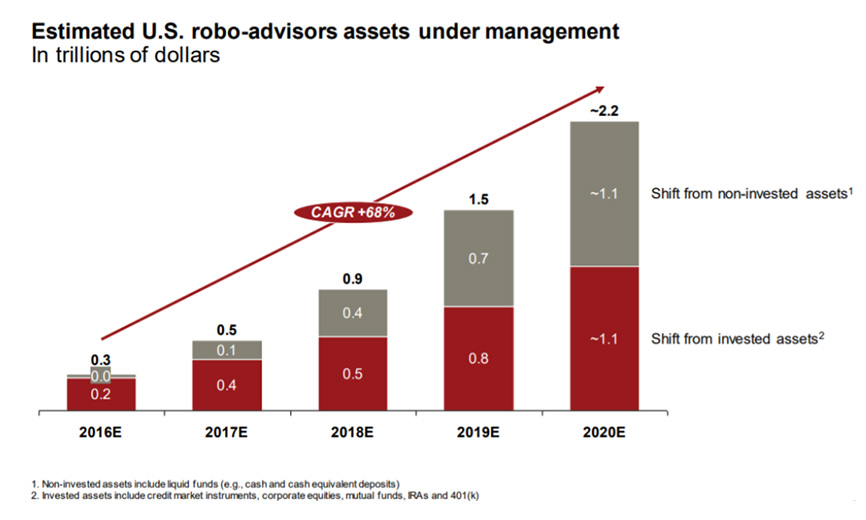

If AUM by robo-advisors continue their CAGR at 68 percent until 2027, AUM by robo-advisors can reach the astonishing amount of $90 trillion (more than the total global assets under management reached during 2016 — $84.9 trillion). Furthermore, companies like Betterment, which focus heavily on robo-advising, have seen an increase in its AUM of more than 100 percent annually during the last five years.

There are at least three reasons why robo-advisors are growing so fast, and why they are a real threat for the traditional wealth management firms.

1) Lower fees

Financial advisors are expensive — while not as expensive as in the past, they continue charging much more than robo-advisor companies. For example, while traditional wealth management firms charge between 1 and 2 percent in management fees (depending on the account balance), robo-advisor companies charge between 0.15 and 0.5 percent in management fees.

2) Similar or higher potential performance

Despite their high fees, financial advisors do not necessarily outperform the market. The number is shocking. According to Financial Times and CNBC, between 80 and 90 percent of active managers underperform the benchmark in a period of 10 to 15 years. Thus, why pay active managers if they perform worse than the market? Robo-advisors, having a passive strategy, can beat active managers, having higher returns for their customers at a lower price.

3) No minimum balance requirement

While some traditional wealth management companies need a minimum balance requirement of $200,000, some robo-advisors don’t need any minimum amount to invest, allowing more people to use their services and to take on less financial risk.

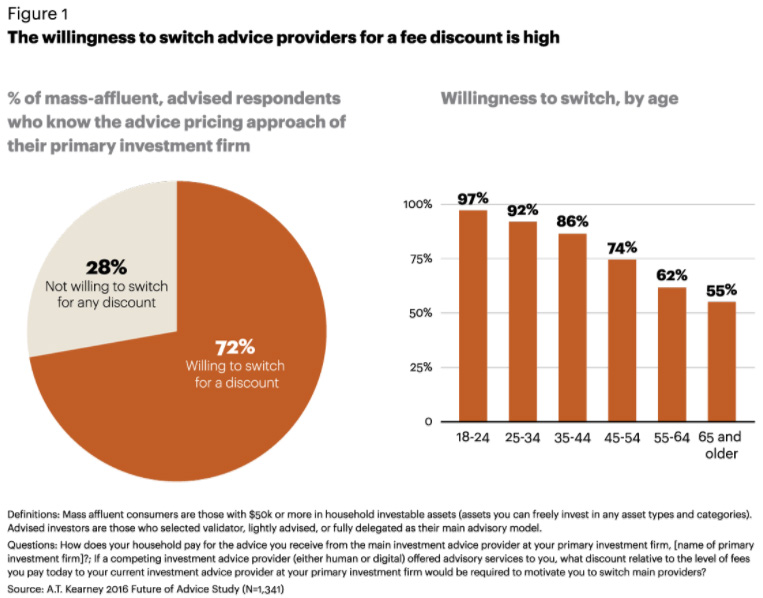

This is not all—there’s more good news for robo-advisors. According to a study done by A.T Kearney in 2016, the willingness to switch financial advisors is more than 90 percent in the age group of 18 to 34.

However, even with all this good news for robo-advisors, there are still some open questions in the industry, such as security, regulation, and how robo-advisors will perform in a bear market. What is true, though, is robo-advisors are not a fad, but a trend to stay. As Ben Alden, general counsel at Betterment, mentioned in his lecture at Cornell Tech, we don’t speak any more about having a smartphone and we generally refer to it as a phone . In the future, we will not speak about robo-advisors, we will just speak about investment.

About Gonzalo Bascur, One-Year MBA ’18

Gonzalo is a management consultant with a passion for finance, financial services, asset management, and fintech. Prior to coming to Johnson he worked as a manager of strategy and operations for PwC in Santiago, Chile.

Comments