Potential leveraged buyout: Our client took the driver’s seat

By Brian Guo, Two-Year MBA ’19

Four months ago…

“What makes a company a strong leveraged buyout (LBO) candidate?” asked my interviewer.

Having not focused on LBO specifics yet, I stuttered: “Um, a company with stable cash flows, margins with expansion potential, lower CapEx spending, ability to support a significant amount of debt, a large asset base to borrow against, and a strong management team.”

The interviewer followed up: “Can you walk me through the mechanics of an LBO or give me an example of one?”

I did not have an LBO deal prepared, so I paused for a few seconds. Finally, I responded. “A leveraged buyout is very similar to buying an investment property [I noticed my interviewer look up from his BlackBerry]… The drivers of return and internal rate of return (IRR) are very similar: entry price, exit price, and timing of cash flows. The equity and debt a sponsoring firm uses to buy a company is similar to the down payment and mortgage a homeowner uses to buy a home. In both cases the bank will look to see if the leverage being applied can be supported by the income generated (Debt/EBITDA) and by the current valuation (EV/EBITDA).”

The interviewer nodded and we moved onto why I was a Lakers fan.

Fast forward to present day

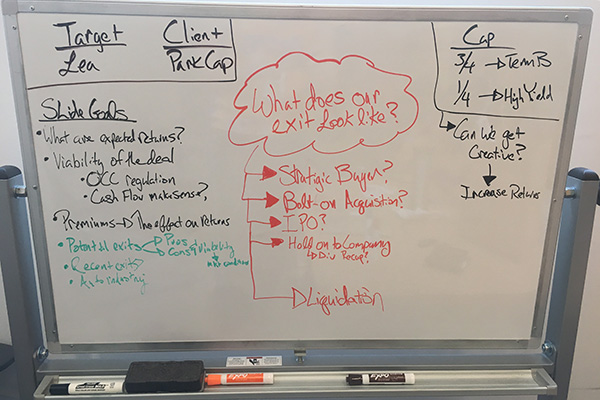

My hands were clenched tightly, pressed against my forehead as if I were praying. I could feel my palms sweating as my vision blurred looking down at the slides I printed out. Why hadn’t I volunteered our team for the first case involving bonds? I understood the investment grade space. Why couldn’t I have been selected to present for the second case, PlayAGS’s IPO? There was a technology portion I was interested in, and I had already followed several IPOs in my past life. Instead, I was anxiously waiting for my team’s number to be called. Waiting to see if we would be presenting our potential leveraged buyout of Lear Corporation, a leading automotive seating and electrical distribution systems manufacturer.

This week we weren’t just presenting to Drew Pascarella, lecturer of finance, and several second-year students—we had special guest Christina Park, MBA ’02, managing director in leveraged finance at RBC Capital Markets. Who better to question and challenge our presentation, than an expert in the leveraged finance markets? If the stakes weren’t high enough, behind our immediate audience were 30+ classmates, all of whom vetted the same case and read the financials, press releases, and analyst reports. From the story to the model, everything in our presentation better jive!

Changing direction on the spot

Drew calls out, “team 11!” That’s our cue. Kevin Chung, Josh Howard, Gyurme Karma, Ben Rashbaum, and I walk up to the front of the room, ready to run through our 11-slide deck.

Drew says, “Given that we’ve already heard several overviews of the auto industry, in the interest of time we’ll just do questions and answers around this deal. Tell us high level if you think Lear is a feasible LBO candidate and three major takeaways.”

We all froze for a split second having just been pushed outside our comfort zones. The security blanket of flipping through our individual sections, so conducive for the divide and conquer method, was just ripped from us. Just like any real client presentation, our agenda was scrapped and the client began dictating the direction of our meeting. However, we quickly recovered and dove into our analysis of Lear, justifying our five-year IRR target between 17 and 18 percent:

- Strong and predictable cash flows

- Healthy asset base

- Stable and mature industry

- Strong management team

We covered ourselves by discussing the potential risks Park Capital (our audience/“client“) might encounter with this LBO.

- How would a sponsor monetize a portfolio company slated to grow to a $22 billion enterprise value in five years?

- Lear’s history with bankruptcy

“What happens to Lear if the economy falls into a recession?” asked Christina Park.

I start speaking about where the economy currently is and what we should expect from a global macro perspective.

“What happens to Lear when the economy falls into a recession?” Christina asks again.

I start rambling about autonomous vehicles and broader industry trends.

Drew follows up, “If the economy falls into a recession, how does that effect Lear’s financials?”

The realization finally sinks in that I have no answer for this question. No amount of tap dancing could bail us out of this situation because as a group failed to model a downside scenario. Such an obvious thing to do, and we completely missed the mark. I could feel my skin turning red as the tension in the room built with each second of elapsing silence. We did the only thing that made sense. We apologized for not having looked at a recessionary scenario, and that we would follow up with the client once completed.

Safe space for mistakes

The stakes are seemingly high in the classroom, but not nearly as high as they are in the boardroom. The reality is we would rather misstep in front of alumni and classmates willing to provide constructive feedback, than falter in front of clients who won’t return our calls going forward.

Following our presentations, Christina provided a great overview of the leveraged finance markets, how she would have approached this case, and how LBOs are actually executed in the real world. Her expertise was truly on display, as students peppered her with questions for more than an hour. The dedication of our alumni continues to surprise me every day at Johnson, and it has been a major component to the success of our investment banking immersion program.

Comments