M&As are Up, IPOs are Down. What’s the Story?

Above: Illustration source: Maravillas Delgado

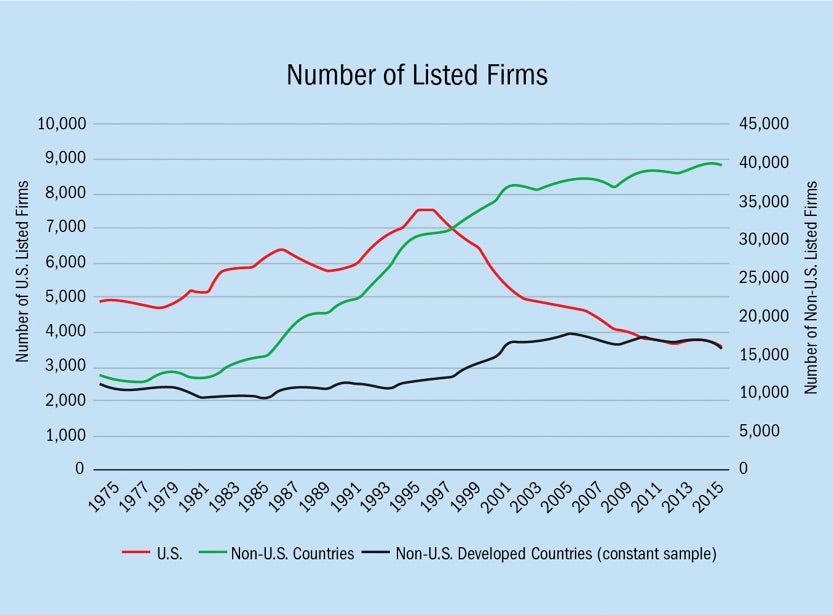

In March 2017, Johnson finance professor Andrew Karolyi and two co-authors published a research study in the Journal of Financial Economics titled “The U.S. Listing Gap.” To Karolyi’s knowledge, it was one of the first widely cited studies that shined a light on a macro trend that had eluded widespread news coverage. Between 1996 and 2012, the paper showed, the number of publicly listed firms in the United States had dropped from 8,025 to 4,102.

The “listing gap” term refers to the number of public firms the authors conclude the U.S. markets should have, ideally, to spur a healthy level of economic and job growth and investment. “The common wisdom out there among classical economists is that a healthy capital market produces a healthy economy. It creates opportunities for companies to enter markets, to raise funds, to invest in future growth, and creates opportunities to hire people, to invest in infrastructure, to expand, and to grow,” says Karolyi.

If the listing gap study pointed out a trend that was hiding in plain sight, the research team’s follow-up publication, “Eclipse of the Public Corporation or Eclipse of the Public Markets?” in the Journal of Applied Corporate Finance (May 28, 2018) exposed the big purple elephant in the room. Karolyi’s “Eclipse” paper not only showed that firms today are less likely to go public; it argued that the U.S. public markets aren’t satisfying the financing needs of “young firms with mostly intangible capital” — or R&D intensive companies.

As the authors wrote, “What we are witnessing is an eclipse, not of public corporations, but of the public markets as the place where young, successful American companies seek their funding.”

In addition to earning a mention in a feature story in The Economist, Tesla CEO Elon Musk referenced it in a tweet to his 21 million followers, catapulting an academic topic into popular discussion. “When you get Elon Musk tweeting and sharing your research with 21 million followers, you feel like you’ve kind of made it on a whole new level,” says Karolyi, who also serves as deputy dean and dean of academic affairs for the Cornell SC Johnson College of Business.

Going Private Through M&A

The availability of private funding — and the regulatory pain of running a public company — has made reluctant public company CEOs like Musk grumble, even as stocks continue to soar. At the same time the debate around Tesla’s ownership status temporarily raged (Musk, aided no doubt by SEC intervention, has since given up his quest to take Tesla private), the U.S. stock market continued to enjoy an extended bull run. Though volatility increased toward the end of 2018, that run had continued despite fewer companies joining the public exchanges and even more firms leaving them, as Karolyi’s paper showed.

Rather than “taking the company private” as Musk might have done with Tesla, most companies “delisting” from the exchanges are doing so as a result of M&A activities, which have also reached their highest levels ever. Since the listing peak in 1997, there have been 8,620 delists, with 61.2 percent of them resulting from acquisitions, according to Karolyi’s research. Only 3.3 percent, on the other hand, were voluntary. The remainder were delistings for cause, mostly due to poor performance.

In the same period (1997–2016), share repurchases and stock buybacks were $3.6 trillion greater than the amount raised from issuing equity over the same period, note Karolyi and his co-authors. That means the companies that remain listed on public exchanges are bigger, older, and have more cash reserves than ever. Until recently, a company with a trillion-dollar valuation seemed inconceivable; Amazon and Apple hit that mark in fall 2018 (although Apple’s value took a deep dive immediately afterwards). Alphabet, Google’s parent company, is not far behind.

U.S. startups are either waiting much longer to go public or getting swallowed up by bigger competitors. According to U.S. Census numbers reported by Quartz, U.S. businesses are aging: About half of them were more than 10 years old in 2016, whereas in 1996, fewer than 40 percent had reached a decade since their founding.

Besides fueling a rash of delistings, M&A continues to feed the world’s largest public companies, supplementing their relatively weak organic growth. On October 28, IBM announced its $34 billion acquisition of Red Hat, an open-source cloud software company. It was just the latest in a string of high-profile M&A activity that includes AT&T’s acquisition of Time Warner, the merger of T-Mobile and Sprint, CVS Health’s merger with Aetna, and Adobe’s acquisition of Marketo.

In all, a record $2.5 trillion in mergers were announced in the first half of 2018 alone (the record-setting rate continued through the third quarter, then slowed toward the end of the year). Public companies have become growth-through-acquisition machines. “To be a successful public company, scale is even more important than ever before,” says Karolyi. “So, for a certain type of growth firm, it’s more appealing now to secure their exit via acquisition than to achieve an IPO.”

Though not necessarily correlated on a one-to-one basis, the decrease in IPO activity and increase in M&A are related. They are both a function and a result of some fundamental changes in the way companies now grow and seek funding. Taken together, they’re causing huge macroeconomic consequences, changing how MBAs approach the recruiting process, altering how bankers and money managers advise clients, and most importantly, affecting how the U.S. economy will adapt to coming currency and interest-rate fluctuations that could lead to the next recession.

New Sources of Capital Spread an Epidemic of IPO Resistance

Young companies used to view going public not just as a rite of passage into maturity, but as a necessary step to access a large volume of relatively inexpensive capital. That’s no longer the case. More growth companies are remaining private for longer, and that has caught the attention of the national news media. In 2018, Inc. magazine launched its inaugural list of Private Titans, “the 1000 largest, most vital American companies that aren’t public,” as the flip side to the long-respected Fortune 500, which ranks the largest public companies. The Inc. list is diverse but includes a noteworthy who’s who of tech growth companies such as Uber, Lyft, Airbnb, Warby Parker, Stripe, and WeWork.

The amount, availability, and diversity of sources of private capital have all exploded in recent years. According to Bloomberg, venture firms have about half a trillion dollars under management, roughly equivalent to all the money raised in IPOs over the last 10 years.

That doesn’t include new — and newly interested — sources of capital.

It’s been nearly two decades since the dot-com boom and bust, and many tech growth companies are now household names. “Capital that was already out there now wants access to tech,” says Anamitra Banerji, MBA ’04, managing partner and co-founder of Afore Capital, a San Francisco-based early-stage venture fund focused on tech. “That includes family offices from all over the world, overseas institutions, corporate VC, and a whole host of other capital sources that have seen proven tech returns and want to get in on them, especially when the opportunity cost of investing dollars isn’t that great elsewhere.” Mobile is now ubiquitous, expanding the pie and helping to drive consistently high returns for investors, compared with other sectors.

The Growth in Private Equity

Chief among those new and growing sources of capital is private equity, which has only grown in power and reach over the last decade. Private equity firms are raising and investing historic amounts of capital, enabling growth enterprises to remain private longer. Through the first three quarters of 2018, U.S. private equity firms invested $508.8 billion across 3,501 deals — a record-breaking pace, according to research firm Pitchbook.

In many cases, private equity firms are even competing with big companies interested in acquiring the same targets. According to a recent Pitchbook study, private equity firms “face increased competition from already cash-rich strategics that received an additional windfall from the recent reduction to corporate taxes.”

Just how big of an increased M&A driver is that tax cut? Although it’s clear many large companies did benefit from the tax cut, it’s hard to tell if the extra cash flow generated is a significant driver of increased M&A, says Drew Pascarella, MBA ’01, senior lecturer of finance at Johnson, who also directs the Investment Banking Immersion. “The tax cut has the potential to drive volume, but there are many other factors to consider,” he says.

One such factor is a whole new asset class private equity has spawned over the last 10 years called “growth equity,” which essentially bridges the gap between traditional venture capital-sized investments and the ultra-large deals private equity has traditionally been known for. The model: invest big dollars in later-stage companies until they reach the scale of huge, modern-era public firms.

Though not huge in terms of IPO volume, the market for private equity-backed exits is growing, running counter to the longer-term trend of proportionally fewer IPOs, according to Pitchbook. With big dollars to invest, private equity firms increasingly specialize in building big, profitable firms ripe for today’s public markets. Between Q1 and Q3 of 2018, 38 private equity-backed companies went public.

“Growth equity is providing a tremendous amount of flexibility in a way that allows founders to get much bigger and more mature without ever having to access the public market,” says Pascarella. “Growth equity wasn’t even around 10 years ago,” he says, adding that it started with tech but now funds companies across multiple sectors and industries. Private equity firms traditionally focused on either early-stage venture capital investments or late-stage leveraged buyout transactions. With more capital available and increased competition in the M&A and VC markets, funding later-stage growth companies became more attractive.

The sheer size of the funds that growth equity firms are raising is fueling their influence. For example, Insight Venture Partners announced the close of its Fund X in July 2018, having raised $6.3 billion, marking the largest-ever private equity growth fund close. Investors continue to pour money into private equity because of “the potential for alpha, and for consistency at scale,” according to McKinsey. While other asset classes underperform, private equity may outperform public markets in the coming years.

The Strategy Behind Staying Private

While a whole breed of firms, particularly those that require large capital expenditures (pharma and manufacturing, among others) still need the volume of capital most commonly accessed in the public markets, the balance seems to have shifted in the United States. “A disproportionately large fraction of U.S.-based firms have assets tied up in intangible form — not property plant and equipment (PPE), but more in the form of accumulated R&D assets and intangibles that stem from more investment in human capital, patents, and other valuable assets, such as for tech firms,” says Karolyi.

Take the online wedding-planning marketplace WeddingWire, founded and run by Tim Chi ’98. A tech-driven firm, WeddingWire facilitates transactions; it doesn’t manufacture products, and so much of its value comes from its intellectual property and its talent. In another time, his firm would have been a natural candidate to go public, but given the availability of capital (his company is backed by growth equity firms Permira and Spectrum Equity), his company took another route. On September 25, 2018, XO Group Inc., the parent company of wedding-planning website The Knot, agreed to be taken private for about $933 million, combining it into a larger company with WeddingWire.

To finance the transaction, WeddingWire is raising about $600 million in debt financing. Assuming all goes well with the new combined company, it will likely go public at a later stage. But during this growth phase, growth equity investors obviously see a more immediate upside through M&A and debt financing than accessing the public markets. Since the transaction hadn’t yet closed at the time of publication, Chi was unable to comment for this story.

Private Equity “Gets” Today’s Tech Firms

Private equity makes it possible to play your cards close to the vest. For companies in competitive spaces, reporting and regulatory requirements essentially broadcast how public companies are deploying their capital, and that can be beneficial for manufacturing companies expanding capacity, for example. But for tech and software-led firms, that level of disclosure seems to be giving away too much strategic intent. As Karolyi puts it, “Private money gets the unique value proposition of firms coming along in this economy, at least more than public equity markets do.” The public markets value consistent profitability, which is harder to attain for tech-driven companies forced to give away strategic intent in their quarterly public filings. That’s less a concern with private money.

Because tech firms often require less capital to scale than some industries, and since that capital is more readily available, it’s changed the calculus for many private firms like WeddingWire.

“At the end of the day, the difference in cost of capital between private and public has diminished,” says Kunal Ghosh, MBA ’03, managing director and portfolio manager at Allianz Global Investors. “Capital in the public equity market was traditionally cheaper than private equity and debt, but no longer. If the cost of capital is low, and firms’ needs are less — and they can avoid the need to disclose, quarterly reporting, and regulators — then it makes sense that they are staying private,” says Ghosh.

But for most technology firms, an IPO is a way for founders to cash in their chips or to create shares to use as a currency for acquiring other firms. For those that do go public, public stock offers not only a great liquidity tool for founders, early employees, and shareholders; it also provides capital for fueling further growth and business model transformation.

How the Decline of IPOs Has Changed the MBA Job Market

The decline in IPOs has changed the game for a number of industries, especially investment bankers. “Anyone in the business in the ’90s remembers [IPOs] fondly,” says Byron Roth, MBA ’87, chair and CEO of Roth Capital Partners, a boutique investment bank that has raised and co-managed more than $50 billion in funding for small- cap growth companies since the early 1990s. “It was a real boom.”

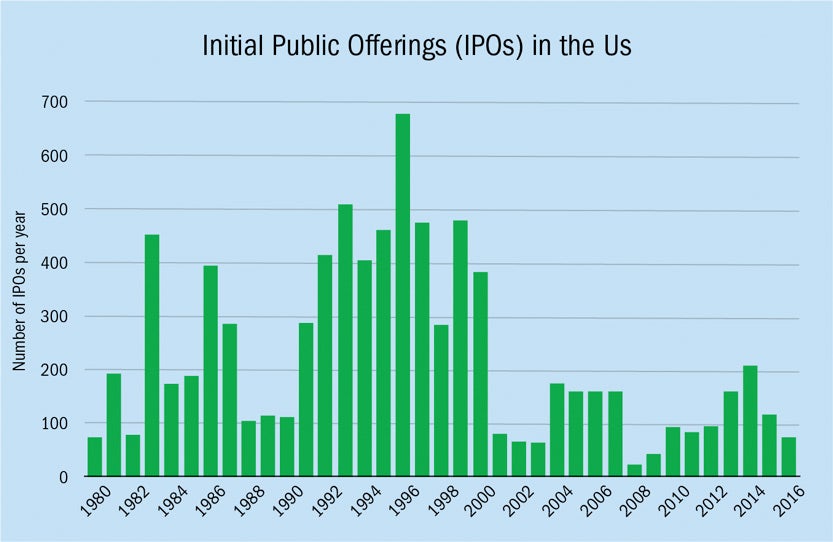

In 1996, when the total number of IPOs peaked at more than 800, Roth says the number of IPOs valued at under $300 million was around 700 — a boon to his firm, which advised the companies and led their public offering, and also to the smaller companies that were able to access the public markets back then. Roth says he doesn’t expect to get back to the IPO volume of the early 1990s, but that the market has improved somewhat from the early 2000s, when his IPO business essentially dried up. Since 2012, his firm leads two to four IPOs a year (down from four to eight at its peak), even as the total number of public firms continues to decrease through M&A.

This shift toward later and fewer IPOs has radically changed the way MBAs view the job market in certain industries. When Katie McGuire, MBA ’17, an associate in Evercore’s oil and gas group in Houston, began her investment banking recruiting process, she was sold on going to a big traditional firm like Goldman Sachs or JP Morgan. At the top of her class, with a leadership seat in the competitive Old Ezra Finance Club and great pre-MBA leadership experience, McGuire looked like a strong candidate for any of the top firms.

But as she got deeper into the process, McGuire realized that some of the luster of the bulge-bracket firms (the largest and most successful name-brand banks), has faded, at least for the MBA set. Fewer companies entering the public markets means fewer IPOs, which have long been an exciting, lucrative draw to investment banking work. In the run up to an IPO, bankers are up against mammoth deadlines, always on a razor’s edge with big payoffs hanging in the balance.

McGuire says about half of the associates in her group in Houston came from bulge-bracket traditional banks like Citi, JP Morgan, Credit Suisse, and Deutsche Bank. Many of them “realized in six months that the IPO equity offerings weren’t giving them the level of experience that they wanted to have,” she says. “When you work the hours we do, it makes a tremendous difference to be working on intellectually stimulating work.” While every M&A transaction is different and custom, big IPOs for established companies can be relatively formulaic and less risky.

McGuire is far from alone in eschewing the bulge-bracket banks.

“When I started teaching at Johnson in 2012, about two-thirds of our investment banking students went to bulge-bracket firms, and the rest went everywhere else,” says Pascarella. “Now, it’s inverted. About two-thirds of students go to non-bulge-bracket firms, and for many of them, the focus is exclusively on M&A. Their firms don’t even execute IPOs.”

While big banks don’t traditionally hire associate-level talent into the M&A group out of MBA programs except with prior industry experience, an emerging set of independent banks like Evercore does. Still, many MBA students value the bulge-bracket brand names, while the independents are still actively building their brands. Though she ended up with multiple offers from bulge-bracket banks, McGuire opted to buck the trend and go with Evercore.

The shift away from bulge-bracket banks is not just driven by fewer IPOs. In many instances, M&A is also more lucrative for bankers. “There’s more money for I-bankers in M&A than in IPOs,” says Pascarella. “If the typical IPO is $100 million and the fee is 7 percent, compare that to selling a company for $500 million, where you earn a fee of 3 percent. M&A offers a more attractive fee opportunity and is generally shared between fewer banks,” Pascarella adds. “When you’re getting paid to raise capital on an IPO, you’re only earning fees on capital raised, where M&A fees are based on the total enterprise value.”

Some bankers who’ve been in the business for a while see the current decline in IPOs as part of a recognizable, ongoing cycle. Alex Ivanov, MBA ’00, managing director in equity capital markets at Citi, is one of them. “If you observe capital markets over a long period of time, there is a cyclicality to the IPO market,” says Ivanov. “Sometimes the public markets are the best way for small companies to access capital, because values are high. At times, M&A can be the best path for private companies to realize value and for larger companies to invest in growth. Over the last 12 to 18 months, the market has been rewarding companies who make smart acquisitions, and the capital markets have been very supportive from a cost-of-capital perspective.”

A Harbinger of Recession to Come?

Still, there are some signs that the “listing gap” could have long-lasting negative effects on the U.S. economy. In a recent appearance at Stanford, SEC Commissioner Kara Stein explained the anticipated effects on the overall market if too many companies stay private. “For starters, more investors could be hurt, since investor protections in the private market are less robust than in the public market,” Stein said. “And as the proportion of private companies grows, there’s less information flowing into the financial ecosystem, reducing the market’s overall transparency,” she says, warning of the long-term economic impacts of such an environment.

While the economy has set records in terms of M&A activity, IPO reluctance, and share buybacks, this isn’t the first time the economy has experienced such conditions. Ominously, in each previous instance, a recession has immediately followed. A big year of deal-making in 1989 preceded a mid-1990 recession, according to the New York Times. It happened again just a few years later. “Companies announced acquisitions worth a then-record $3.4 trillion in 2000, and within three months the dot-com bubble had burst and the United States economy had fallen into recession,” reported the New York Times. “Seven years later, merger activity hit another record, topping $4.1 trillion, but the economy had already slipped into recession as the year came to a close.”

Given the current level of M&A frenzy combined with rising interest rates, a looming trade war with China, and continued political turmoil, the same fate looks likely to some experts. Upward pressure on interest rates and downward pressure on the dollar, for example, could cause significant economic headwinds to form, says Ghosh of Allianz Global Investors. At that point, the public equity markets will have a smaller pool of big firms for the investing public to rely on. Asked if he expects these factors to bring on a recession in the near term, Ghosh says simply: “Most probably.”

Article Information

- Categories

-

- Accounting, Economics & Finance