Open for business: China’s financial liberalization

By Raheel Hirji, MBA ’20; Clarence Ho, MBA ’20; Ryan Hoffman, MBA ’20; and Takeshi Honda, exchange student from ESADE Business School

A brief history of China’s liberalization/opening-up

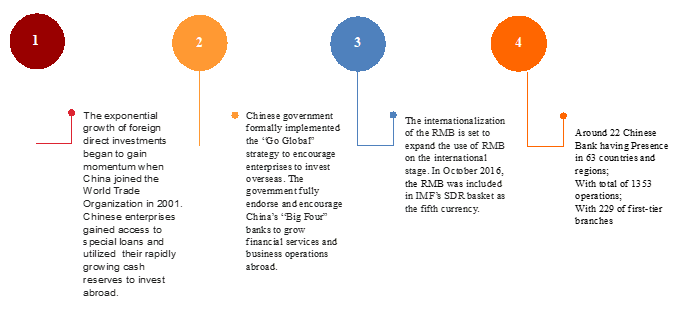

It is no coincidence China has grown to be the second largest economy in the world, all since it made the fateful decision to open up its financial system to the rest of the world. In 1979, China lifted the ban on entry of foreign banks. Only it was at the turn of the millennium as China joined the World Trade Organization (WTO) in 2001 that explosive growth erupted. Chinese enterprises would gain access to special loans and leverage rapidly expanding cash reserve for further investment, pledging in 2006 to open up its banking sector completely. By 2011, the number of foreign banking institutions in China grew to nearly 400. Today, China’s banking system and economy prove ever more globalized and formidable.

Meanwhile, the Chinese government implemented other strategies to spur globalization such as the “Go Global” directive to encourage enterprises to invest overseas, endorsing and encouraging China’s “Big Four” banks to grow financial services and business operations abroad, as well as the internationalization of the Renminbi, all to expand the country’s presence on the international stage.

China’s evolving regulatory network

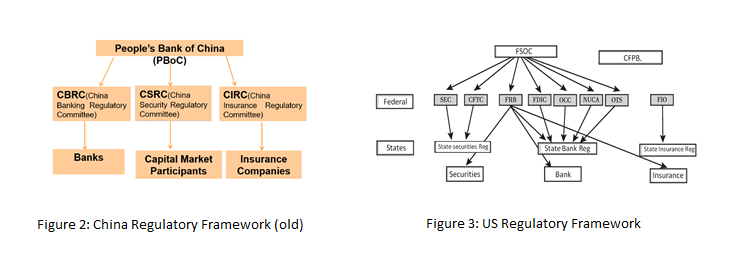

China’s government reshuffled the country’s financial regulatory structure in 2018, which then consisted of one central bank (PBOC) and three committees (CBRC, CIRC, and CSRC), overseeing commercial banks, insurance companies, and capital market participants, respectively. With reform, CBRC and CIRC merged to form CBIRC, relinquishing some rule-making and macro-prudential powers to the PBOC central bank relative to its predecessors CBRC and CIRC.

China’s original regulatory framework was already much more streamlined than that of the United States, with eight regulatory agencies with authorities limited in scope. With the even more centralized financial regulatory structure in China following the merger, China’s government is poised to more quickly address systemic risk in the financial system, especially given the relatively substantial shadow banking sector in China. Another reason for the establishment of the CBIRC was to better coordinate the regulatory activity of both the CRBC and CIRC, as banks in China become more diversified in their business operations.

Although a stronger regulatory agency might seem contrary to financial liberalization, the new combined CBIRC reflects the broader context of China’s “opening up” of the economy. For the government, the reforms to the financial system were designed to contain risks and improve efficiency of financial intermediation without jeopardizing economic stability, which Beijing views as closely intertwined with political stability. As a result, China has taken a gradual approach to financial liberalization as to avoid the mistake of Latin America and some European countries, where swift deregulation resulted in massive debt-fueled growth and asset bubbles that contributed to debt crises. As China emboldens foreign financial firms to participate more extensively in the financial sector, especially in the areas of wealth management and capital markets, a more streamlined regulatory framework arose to respond to the increasing complexity of the financial system.

Likewise, PBOC central bank gained more regulatory responsibilities during the reorganization. Unlike most central banks around the world, PBOC is not fully independent. Although the PBOC has a governor to manage the daily operations of the bank, the policy direction of PBOC is set by the party chief in alignment with the agenda of the government. The appointment of reformist Guo Shuqing is a strong signal that China is committed to continued financial liberalization.

Chinese banks and RMB globalization

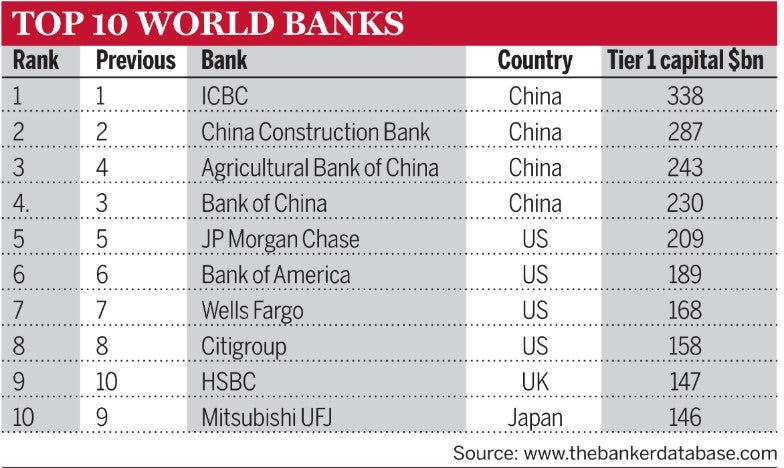

China has a robust banking system where the four largest banks in the world are all Chinese. The Industrial & Commercial Bank of China, China Construction Bank Corp., The Agricultural Bank of China, and the Bank of China are the four largest banks in the world by assets. Despite the impressive size of China’s banks, they are all still evolving. For now, China’s banking system is highly reliant on interest income as a percentage of revenue, accounting for 76%, which is still quite high relative to US banks. Some would argue that it would behoove Chinese banks to diversify their business into more fee-generating lines of business, such as asset management and investment banking.

The internationalization of the RMB is rapidly catching on. As China liberalizes its banking sector, demand for the RMB grows. In October 2016, the RMB was included in the IMF’s SDR basket as the fifth currency. Among liberalization initiatives, the government is in the process of lifting foreign ownership controls, opening its capital markets to foreign banks, and lowering the entry criteria for foreign institutions. In June 2019, the CSRC amended the QFII/RQFII rules to facilitate foreign participation in China’s capital markets.

Overall, liberalization should enable China’s financial system to receive an influx of foreign capital and expertise, with some foreign banks increasing their presence and penetration in high-growth markets – especially for those needing to launch RMB businesses. Such initiatives will continue to drive the RMB’s status as a major global currency.

Key challenges facing Chinese banks

Chinese global banks have to overcome some issues in order to keep growing their business in future.

- Capacity of regulatory compliance in line with capacity of overseas business expansion

- Conservative financial risk appetite limiting the efficiency of business operations

- Overseas customer service falling short

- Further enhancement of technology capacity and investment

- Further strengthening of competitive advantages

About the authors:

Raheel Hirji, MBA ’20, is a full-time MBA candidate at Johnson. Post-MBA, Raheel intends to pursue a career in equity research.

Clarence Ho, MBA ’20, is passionate about hardware technologies, especially in consumer electronics and automotive space. Post-MBA, Clarence would like to work in strategic finance within the tech industry.

After completing his MBA program, Ryan Hoffman, MBA ’20, will be joining Bank of America as an investment banking associate.

Takeshi Honda is an MBA candidate at the ESADE Business School in Barcelona, Spain. Currently, enrolled at the Johnson through its exchange program. Before pursuing an MBA, Takeshi worked at a management consulting firm in Japan for eight years. Main fields were creating business strategies for mid-cap companies and business due diligences of private equity investments.

Article Information

- Categories

-

- Global Development & International Business

- Inside SC Johnson

- Tags

-

- Globalization

- Faculty Areas

-

- Accounting