Indian SMEs: Overcoming funding challenges amidst a global pandemic

Indian SMEs, an eternal underdog

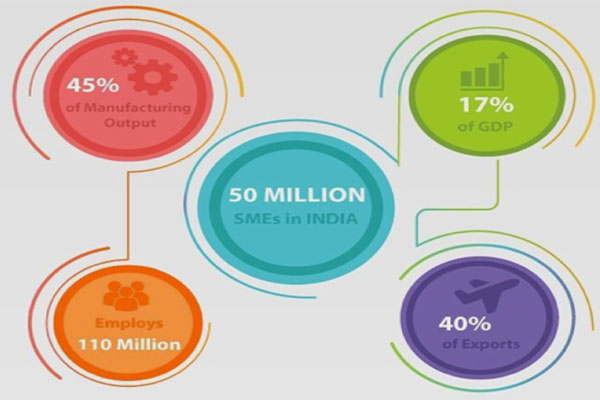

Small and Medium Enterprises (SMEs) are companies with estimated revenues between $20 million to $250 million. With 50 million SMEs, India accounts for the second-largest number of SMEs in the world; only China has more. The pre-COVID up-turn of the SME segment was a silent revolution that had fueled the Indian economy for the last three years, off-setting the lackluster performance of the large-cap segment and contributing to the 6 percent to 7 percent annual growth. This emergence of a largely underestimated segment is also gaining global prominence, with the World Bank now estimating that the Indian SMEs are expected to constitute approximately 80 percent of the industrial ecosystem, employ approximately 110 million people, and contribute more than 45 percent of manufacturing output.

Historically, the segment has recorded a double-digit compound annual growth rate and has contributed about $600 billion in gross value to the Indian economy annually. The advent of technological platforms such as social, mobile, analytics, and cloud (SMAC), and their subsequent adoption is expected to further supplement growth by at least 30 percent, propelling the segment to reach $1 trillion in the next three to five years.

Positive outlook despite strong COVID headwinds

Even in the wake of a global pandemic, SMEs remains resilient and relatively more confident of surviving the existential crisis following the COVID breakout and lockdown. Engaging with ex-clients in India revealed that a majority of them are confident of surviving the current downturn and are in evidently better financial and operational holding as compared to their peers in Asia. In fact, a healthy 61 percent of Indian SMEs claimed that they would thrive in their operations in the post-COVID world. With significant public and private sector initiatives, including “Make in India,” Indian SMEs have a ready base to deliver the right product, the right quality, the right solution, and the right service at a competitive price, both in domestic and international markets.

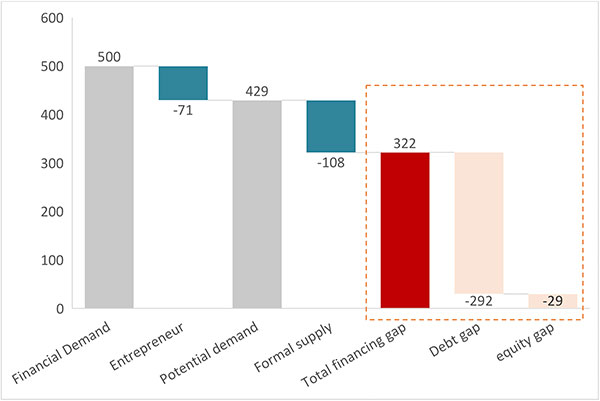

$300 billion demand supply funding deficit

Despite their growing importance in the economy, SMEs are plagued by certain inherent handicaps that have proved to be a constant obstacle in their efforts to emerge as a true growth phenomenon. Chief among these obstacles is the lack of a steady flow of growth capital. SMEs remain underserviced by financial institutions despite their critical place in the economy, resulting in a funding deficit that has accumulated to more than $300 billion. This is the trend that shocks me. Over the last five years, working with more than 25 SME clients, I have experienced the growth challenges prevalent in the segment. The financing deficit bothers me because I have seen its first-hand impact on curtailing non-tech entrepreneurship, employment generation, and growth.

I believe the fragmented and territorial nature of SMEs, together with information asymmetry (a lack of verifiable data sources, like Traxcn) is a major reason why investors are unable to build consensus or support capital infusion. Further, primitive credit evaluation processes adopted by lending institutions, which avoid a comprehensive analysis of accurately estimating risk, has resulted in a lack of debt capital inflow. Another factor that thwarts capital flow into the segment is the investor’s sheer disinterest, caused by a common stereotype that SMEs are “bad” customers to lend to because of the smaller transaction size and higher risk perception, generated primarily by limited market data and intelligence.

Addressing capital gaps through innovative risk modeling and technology adoption

Technology and financial innovation, together with the use of innovative data sources for risk assessment, will play a pivotal role in reversing the capital deficit trend.

The rapid adoption of technological solutions such as data analytics can improve information availability to facilitate data-driven decision-making for lenders and investors. Simultaneously, with digital empowerment, SMEs would be able to improve operating performance and generate verifiable data for evaluation. Cumulatively, digitization will improve transparency, information flow, and enable business case evaluation for creating compelling investment propositions and thus improve financing.

Traditionally, risk modeling used to be the preserve of large financial institutions, entrenched requirements, and constraints leading to static models. Only a small set of SMEs have been rated by credit agencies, while many have been excluded on a prima facie basis. However, newer risk models are dynamic and adopt machine learning to become smarter, which is a significant advantage over traditional models that rely on processes and regulations that were more time-consuming and left many out of reach of essential operating credit. The transition from older to newer risk models will also allow investors to better securitize their investments with low-risk bundling.

Fintech-driven AI platforms will further bridge the SME funding gap. These financiers—who use non-traditional data sources such as daily point-of-service collection to gauge consumption, spend on SMEs’ product categories, and AI-based algorithms—will break away from traditional credit stereotypes and evaluate SME potential and opportunities accurately to finance growth.

Finally, innovative financing instruments such as tiered disbursal schedules and performance-linked debt and equity repayment plans will contain risk and maximize investment potential to bridge the segmented capital deficit.

While technology adoption will help bridge the capital deficit and improve operational and financial efficiency, I believe the fundamentals of the segment remain extremely strong. With huge commitments from the government and increased emphasis on a self-reliant India, innumerable SME opportunities are expected to thrive. However, strategic technological outlook, speed, and precision to overcome the economic uncertainty will have a serious bearing on how the segment emerges from the lockdown.

The fighting spirit of the Indian SME segment has been tried and tested across decades of financial and economic downturns. With an increased emphasis on creating and adopting a sustainable technology infrastructure that will augment an incremental inflow of growth capital to the segment, the Indian SMEs will be primed for multifold growth in the post-COVID era.

Comments