Emerging markets champion: CEMEX, a Mexican global company

By Abdellah Bouhamidi, One-Year MBA ’19 and EMI researcher

In each of Professor Casanova’s emerging markets classes, we discover companies from emerging economies that compete head-to-head with giants from developed nations, despite the multiple disadvantages the former face intrinsically within their domestic markets (lower purchasing power, harder access to financing options, currency volatility, etc.). This post presents another stunning success story of an emerging markets champion; CEMEX is a leading global producer of cement, ready-mix concrete and aggregates; fifth largest in the world and second in North America by revenue; third by available production capacity, with global operations in all continents.

Paving a way to the podium

CEMEX dug its way to the leaderboard, from being a small private cement-focused local company facing fierce competition in its home market to becoming an innovative publicly-traded global leader in 25 years. This ascension wasn’t clear from complications and obstacles: Mexican crash, U.S. anti-dumping penalties, recessions, competition, high debt and rating downgrade all stood in the way of CEMEX, but the Mexican company knew how to turn these around into advantages and to build a strong foundation from these experiences. This raised a lot of curiosity and questions in class, and students were mainly curious to know:

- How did CEMEX reach such global heights?

- What did it take the company to make it to the top?

- And whether or not this expansion model would still be viable in the future?

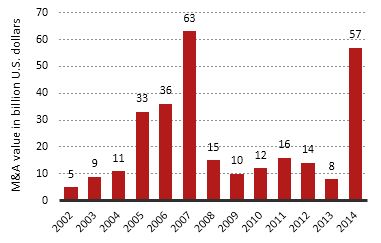

Cement, a $400 billion jackpot

Cement has known a tremendous growth – demand doubled between 2002 and 2011 to reach 3,577 million metric tons – driven mainly by increased housing and Infrastructure needs. The global market is only shared by few dominant players, due in part to a wave of Mergers and Acquisitions (Figure below) that characterized the last 18 years. If the market size was estimated to be a hefty $395bn in 2017, it is projected to reach $682bn at a CAGR of 7.8% by 2025, and CEMEX currently takes home about 7% of this pie.

The CEMEX way

CEMEX’s success started in 1989, when the company decided to acquire Tolteca, their main competitors in Mexico, and consolidate its position in the Mexican market. The first internationalization step was to Spain (1992); then Venezuela (1994); the Dominican Republic (1995); Colombia (1996) and the Philippines, Indonesia, Egypt, Chile, Costa Rica (1997-1999).

CEMEX played a combination of “ruthless operating efficiency” (a catch phrase used within the company), innovation in new capabilities and growing global presence and relationships to raise capital at low rates and to gain leverage during their mergers and acquisition spree. This strategy has helped the company have a foothold in every continent (more than 50 countries), a move that enabled it to hedge currency fluctuations effectively – a major factor that could hinder EMNCs’ growth – given that 50% of its revenue comes from North America and 50% from other places of the world.

Stress, strain, and cracks

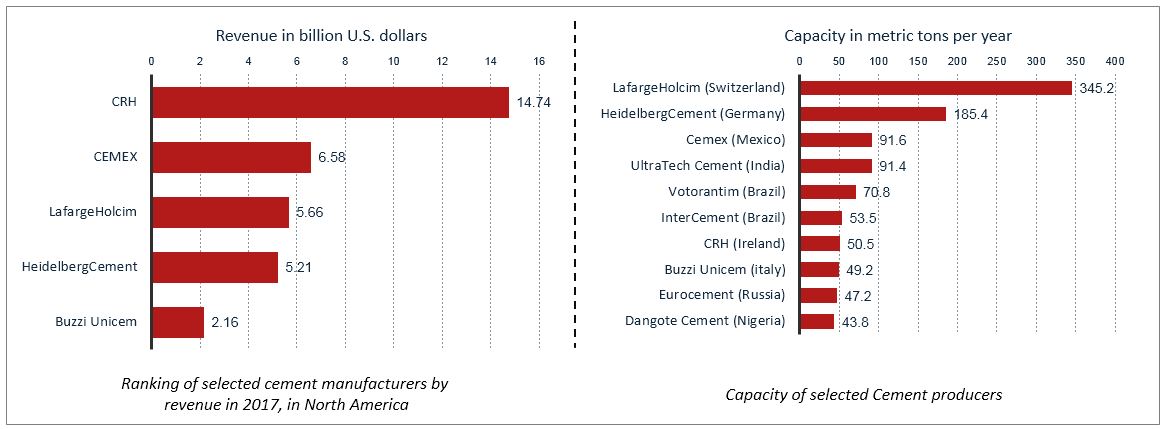

One of the strategic focuses of CEMEX, taken from their annual report, is to seek “value before volume”. And this is the best direction to steer the company to, given a visible gap between current capabilities and potential to capture more value/consumer surplus: CEMEX is third worldwide by production capacity, but only fifth by revenue, and is topped in North America by CRH, an Irish company whose 7th by capacity but first in the region by revenue, double that of CEMEX (See figure below).

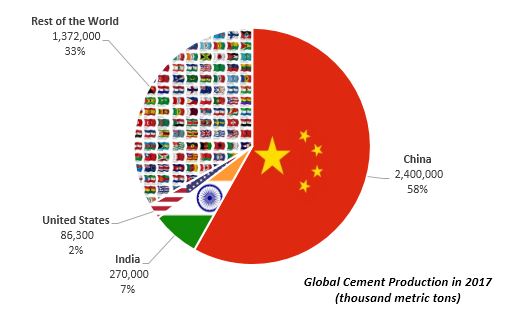

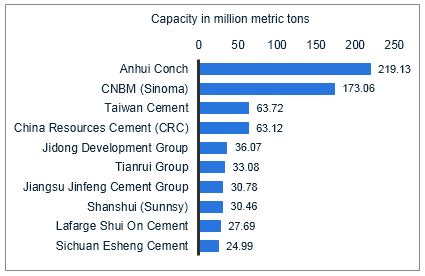

On the other hand, we can also foresee a hard time in the cement industry for companies seeking value and differentiation in the future. With China’s production capacity, as is apparent from the statistics (figure below) we see that China produces around 60% of world cement and clinker with about 2 billion metric tons. And even though the Chinese government has recently restricted the expansion of capacity on a range of industries that include construction materials, and proceeded to destroying any excess production, the reason mentioned for this regulation is power shortage and outbreaks during winter, so that leaves doubt as to whether this is a permanent restriction or a temporary hold until an alternative solution to energy is laid out. Also, this new regulation still allows room for capacity to be replaced; e.g. installation of modern and efficient equipment and facilities… In other words, as we know of Chinese companies in general, Chinese cement producers – of which the top 10 locals alone hold a capacity level close to the top 10 global companies by revenue – would not much be interested in profit, but rather more in the top line and in international extension. Adding the previous two elements together further supports prediction that there would be an increased price pressure on the market in the near future, which in my opinion poses the main threat, along with the level of debt that CEMEX has to manage, after the company enjoyed successful years acquiring its contenders. Beyond this point, I would see it harder and more complicated (this applies also to competitors) to use the same M&A formula again given the current combination of events, and the degree of consolidation this industry has come to.

Sources of growth

Unused production capacity, Industry consolidation, high or nearly plateaued urbanization rate are major elements that would limit growth in the cement industry. Under these constraints, the main concern that pops up is how can producers seek and sustain value? Particularly, what would be a viable strategy for CEMEX moving forward? A number of options were presented and discussed in class, ranging from: reduce leverage and count on organic growth, pursue M&A in emerging markets or focus on BRIC countries, to: take over companies in developed markets, with pros and cons of each endeavor. Besides all these options, as an operations researcher and firm believer in internal innovation as a major source and driver for growth, I believe two options would have significant results: (1) innovating in new solutions such as modular construction, prefabricated and ready to assemble elements, and (2) downstream vertical integration, and here I am thinking more about the forefront of the value chain: infrastructure and housing construction and brokerage, as Samsung and other companies are doing in emerging markets.

About Abdellah Bouhamidi, One-Year MBA ’19

Data scientist and operations research specialist, Abdellah worked for five years delivering data, solutions, and recommendations to decision makers from the private sector, central government departments, and global firms willing to invest in Africa and the Middle East. He worked as a consultant and analytics manager in Casablanca and co-founded an online private sales startup before joining the Emerging Markets Institute as a researcher in 2017. He enrolled in the One-Year MBA program in 2018. Abdellah is mostly interested in using digital technology and artificial intelligence for clean economy/systems, transparent governance and education applications.

Article Information

- Categories

-

- Inside SC Johnson