The CFA franc, a modern-day colonial system

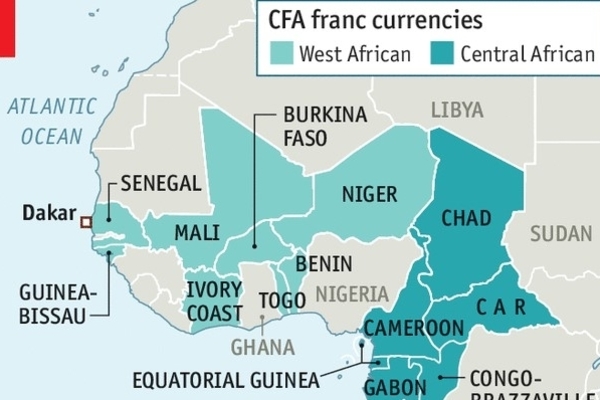

“Françafrique” refers to France’s sphere of influence over its former colonies in sub-Saharan Africa. Militarily, France has intervened more than 50 times in its former colonies since independence in the 1950s, often for the protection of local regimes. These fourteen countries form a currency union called the Communauté financière d’Afrique (CFA) or Financial Community of Africa. Prior to the wave of independence, the currency was known as Colonies Françaises d’Afrique, and while the name has changed, the same punitive, illegal colonial system remains to this day and continues to deprive African nations of their prosperity.

Former French president, Jacques Chirac, said in 2008: “Without Africa, France will slide down into the rank of a third [world] power,” echoing a 1958 publication of Politique Française et Abandon, when his predecessor François Mitterand warned that: “Without Africa, France will have no history in the 21st century.”

What follows is my reflection on the continuities and discontinuities of this system at this moment of reckoning.

The last colonial currency

Debates over the use of the CFA franc weighs heavily on African states’ sovereignty. The intention behind the 75-year-old colonial French policy of splitting its colonies in Africa into two currency zones—the West African Economic and Monetary Union (WAEMU) and the Central African Economic and Monetary Community (CEMAC)—was to facilitate France’s import of goods from its colonies, obtaining unilateral access to raw materials in the region in exchange for stability and economic ties. In practice, the suspicion of neocolonialism would grow over the years across the region. Following a period of economic stagnation in the CFA region in the mid 1980s and 90s, with the support of the IMF, Paris exercised its colonial powers to devalue the currency by a whopping 50 percent and to allegedly boost the exports of its former colonies so as to compete on a global level. What followed was a wave of price increases, demonstrations, and violent clashes all over Francophone Africa. The CFA franc is among the legacies of colonialism and remains more beneficial to the European Union (EU) than to Africans.

An iron-clad colonial monetary system

- A currency printed in Chamalières, France by the Banque de France since its inception in 1945

- A monetary system pegged to the EURO since 1999 and to the French franc prior

- French officials maintain veto power on the board of both regional central banks

- Member countries retain at least 50 percent of their foreign exchange reserves with the French treasury

- Total reserves estimated to be north of $15 billion as of November 2019 with a fixed 0.75 percent interest rate at the Bank of France

- Both CFA currencies are pegged to the euro but are NOT interchangeable; further prohibiting intra-African trade

Through its veto power in the central banks of the CFA zone, France is still in the position to control the region’s financial and monetary regulations, money supply, and credit allocation, depriving the region of proper and basic institutions and compounding the region’s instability.

Benefits of the CFA franc

Supporters of the CFA franc are mainly composed of the French Ministry of the Economy and Finance as well as French-backed CFA presidents. Their position is that the CFA provides monetary stability to a region of the world known for its history of wars and coups. The peg to the euro guarantees a stable exchange rate providing certainty with pricing. In addition, CFA countries enjoy low inflation relative to its African neighbors. Côte d’Ivoire, for instance, experienced an average inflation rate of 6 percent in the last 50 years, much lower than its anglophone neighbor Ghana, which averaged 29 percent.

And yet, it is evident that the EU stands as the greatest beneficiary of stable prices. Prior to independence, local farmers were bound to exclusive agreements that included prices that favored French interests. Not much has changed since.

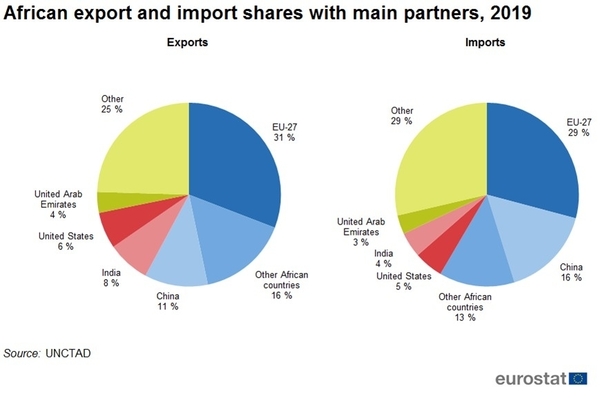

2019 EU-Africa trade statistics:

- 70 percent of goods exported from the EU to Africa were manufactured goods

- 65 percent of goods imported to the EU were primary goods (food, raw material, and energy)

- France (€27 billion), Germany (€24 billion), Spain (€19 billion), the Netherlands, and Italy (both €17 billion) were the largest exporters of goods to Africa in 2019

- The five largest exporters were also the largest importers of goods from Africa in 2019

- Spain (€27 billion) led, followed by France (€24 billion), Italy, Germany (both €21 billion) and the Netherlands (€16 billion)

Companies dominating critical sectors in the CFA region:

- Total (France; energy)

- Bouygues (France; public works & buildings)

- Bolloré Group (France; rail, sea, and transportation)

- Orange (France; telecom)

- LafargeHolcim (France; cement)

Local CFA region companies are hard pressed to compete with their French counterparts. In many cases, when local companies are involved in major projects it is in the form of joint ventures where the multinational company (MNC) brings its capital, expertise, and equipment in exchange for local influence. Given the outsized sway these MNC’s hold over African politics, the above companies have long secured their African markets without making a tender. For example, in 2018 French billionaire and head of Bolloré Group, Vincent Bollore was arrested over allegations he indirectly influenced election outcomes for governments in West Africa in return for lucrative port contracts.

It should be noted that China has emerged as a viable alternative to the former colonial powers as it has become the largest single source of loans for African nations. From 2000 to 2017, the Chinese government and banks signed $146 billion in loan commitments to African governments but is facing criticism for its “debt-trap diplomacy” as loans are mostly backed by natural resources.

Reality of the CFA franc

The stability of the currency is a double-edged sword. By requiring half of the foreign reserves to be stored in the French treasury, the former colonial power limits the liquidity available to spur economic growth and build necessary infrastructure such as hospitals, schools, roads, and power plants to build industry, agricultural, and manufacturing capacity. The liquidity crunch is felt by small and large businesses alike hard pressed to access credit and sufficient funding for projects and working capital. Further, the peg to the euro holds the region’s central banks hostage to the monetary policy of the European Central Bank, which essentially sets interest rates for the CFA zone, further restricting the region’s economic autonomy.

With the fastest growing population in the world, Africa is poised to boom between now and 2050, but the unemployed youth would have most to lose should the colonial system perpetuate. Other movements such as like Y’en a Marre in Senegal and Le Balai Citoyen in Burkina Faso, demand the abolishment of the CFA zone. Perhaps the most controversial figure in this debate is Benin-born French activist, Kemi Seba, known for his social media campaigns who have mobilized thousands of Africans across the continent. Indeed, among African youth, we are beginning to see signs of change.

Business (not) as usual

As pressure continues to build, Paris is seeking to reshape its relations with its former colonies. In this manner, in the past year President Macron of France has agreed to change the name of the CFA franc (once again), loosen the central bank’s foreign reserve requirements, and vacate its board seats at the central banks on the condition that the currency remains hard pegged to the euro. But it may be too late. Nigeria now leads an effort to oust France from the region completely in negotiations around the Economic Community of West African States (ECOWAS) and around the long-term plan for a common currency, bringing the French system ever closer to its overdue conclusion.

1 Comment

Auguste TAMEZE

Very nice my son…I am so proud of you

Comments are closed.